All Categories

Featured

Table of Contents

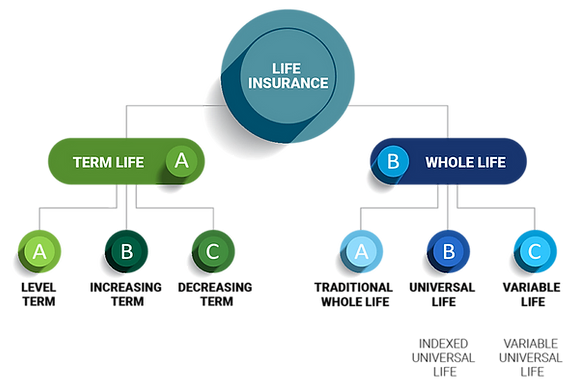

Level term life insurance policy is a plan that lasts a set term generally between 10 and thirty years and features a level fatality advantage and degree premiums that stay the exact same for the entire time the policy holds. This indicates you'll recognize exactly how much your payments are and when you'll have to make them, permitting you to spending plan appropriately.

Degree term can be a wonderful option if you're seeking to buy life insurance policy coverage for the first time. According to LIMRA's 2023 Insurance Barometer Research Study, 30% of all adults in the U.S. demand life insurance and don't have any kind of kind of policy yet. Degree term life is foreseeable and economical, which makes it among the most prominent types of life insurance policy.

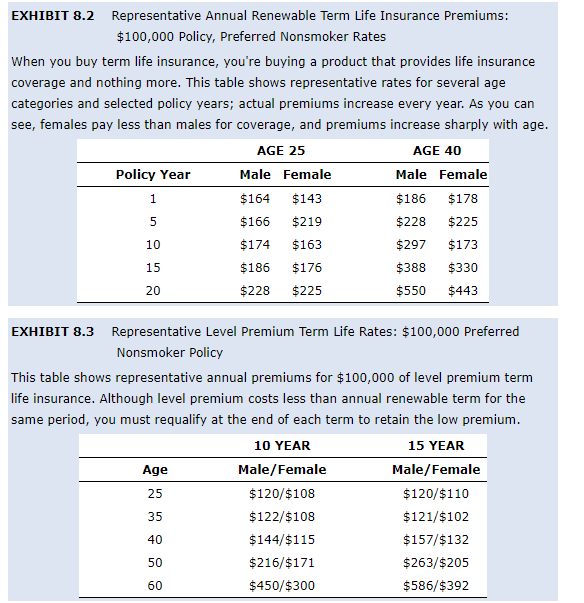

A 30-year-old male with a similar account can expect to pay $29 per month for the very same coverage. AgeGender$250,000 coverage amount$500,000 coverage amount$1 million protection amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Method: Average month-to-month rates are computed for male and female non-smokers in a Preferred health category getting a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy plan.

Prices may differ by insurer, term, insurance coverage amount, wellness course, and state. Not all policies are readily available in all states. Price illustration valid as of 09/01/2024. It's the cheapest form of life insurance for a lot of people. Level term life is a lot more affordable than a comparable entire life insurance policy policy. It's simple to take care of.

It allows you to budget and strategy for the future. You can conveniently factor your life insurance policy into your budget plan because the premiums never ever alter. You can prepare for the future just as easily due to the fact that you understand precisely just how much cash your liked ones will certainly get in case of your absence.

What is Joint Term Life Insurance? Explained Simply

This is true for individuals who stopped smoking cigarettes or who have a health and wellness condition that settles. In these situations, you'll usually have to go with a brand-new application process to get a better rate. If you still require insurance coverage by the time your level term life policy nears the expiration day, you have a couple of options.

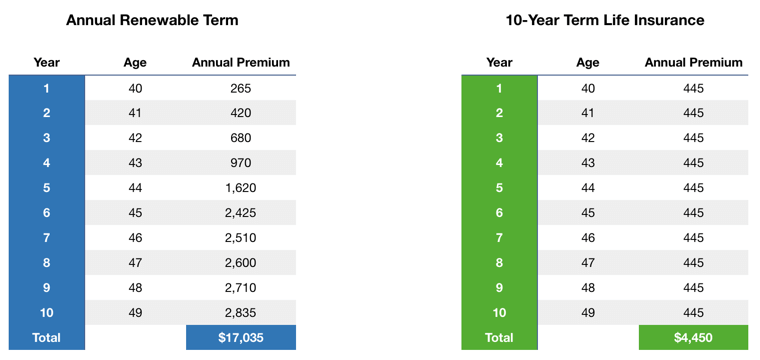

Many level term life insurance policy plans come with the alternative to renew insurance coverage on a yearly basis after the initial term ends. The price of your plan will be based on your present age and it'll raise yearly. This can be a great alternative if you only need to prolong your protection for a couple of years or else, it can obtain expensive quite quickly.

Degree term life insurance is just one of the least expensive insurance coverage options on the market due to the fact that it provides fundamental security in the kind of survivor benefit and only lasts for a collection amount of time. At the end of the term, it expires. Entire life insurance policy, on the other hand, is dramatically a lot more pricey than level term life since it does not expire and comes with a cash worth attribute.

Rates may differ by insurance provider, term, coverage quantity, wellness class, and state. Not all plans are readily available in all states. Rate image valid as of 10/01/2024. Level term is an excellent life insurance coverage option for the majority of people, yet relying on your coverage requirements and personal circumstance, it might not be the very best fit for you.

This can be a good choice if you, for instance, have simply quit smoking and need to wait two or three years to apply for a degree term policy and be qualified for a lower price.

With a decreasing term life policy, your survivor benefit payment will certainly decrease in time, but your settlements will certainly stay the very same. Reducing term life plans like home loan defense insurance coverage usually pay out to your loan provider, so if you're searching for a plan that will pay to your loved ones, this is not a good suitable for you.

Is Voluntary Term Life Insurance the Right Choice for You?

Raising term life insurance policy plans can help you hedge versus inflation or plan economically for future children. On the other hand, you'll pay more in advance for much less protection with a raising term life policy than with a degree term life plan. Annual renewable term life insurance. If you're not certain which sort of policy is best for you, dealing with an independent broker can help.

Once you've determined that level term is best for you, the following step is to buy your plan. Right here's how to do it. Determine just how much life insurance you require Your protection amount need to offer for your family's lasting monetary requirements, consisting of the loss of your earnings in case of your death, along with debts and daily expenditures.

The most popular kind is currently 20-year term. A lot of companies will certainly not sell term insurance policy to an applicant for a term that finishes past his or her 80th birthday celebration. If a policy is "renewable," that suggests it continues active for an extra term or terms, up to a defined age, also if the health and wellness of the guaranteed (or various other elements) would certainly trigger him or her to be denied if she or he got a new life insurance policy policy.

So, premiums for 5-year renewable term can be level for 5 years, then to a brand-new price mirroring the new age of the guaranteed, and so on every 5 years. Some longer term policies will certainly ensure that the costs will certainly not enhance throughout the term; others do not make that guarantee, enabling the insurer to increase the price during the plan's term.

What is Level Premium Term Life Insurance and How Does It Work?

This implies that the policy's owner can transform it into an irreversible kind of life insurance policy without additional evidence of insurability. In most sorts of term insurance coverage, consisting of property owners and car insurance coverage, if you have not had an insurance claim under the plan by the time it expires, you obtain no refund of the premium.

Some term life insurance policy consumers have actually been miserable at this end result, so some insurance firms have actually produced term life with a "return of costs" feature. The costs for the insurance coverage with this feature are often dramatically greater than for plans without it, and they usually need that you maintain the plan in force to its term or else you forfeit the return of premium benefit.

Degree term life insurance policy premiums and fatality benefits stay constant throughout the plan term. Level term life insurance is normally much more budget-friendly as it doesn't construct cash money worth.

While the names commonly are made use of reciprocally, degree term insurance coverage has some vital differences: the costs and survivor benefit stay the same throughout of protection. Level term is a life insurance policy plan where the life insurance premium and fatality advantage stay the exact same for the duration of coverage.

{kind=link}

Latest Posts

Senior Final Expense Benefits

Funeral Cover Companies

Funeral Insurance Over 60